Transport biofuels

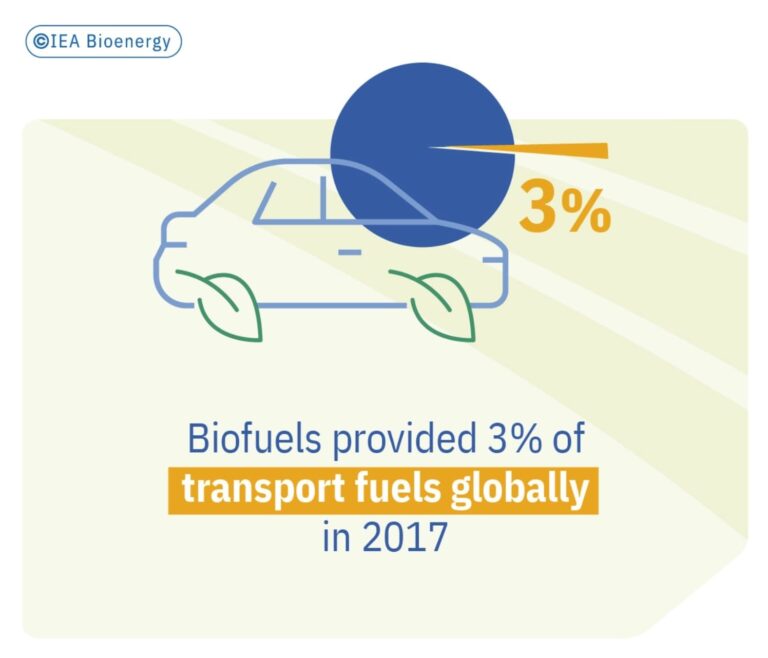

Sustainable transport biofuels are already offering low carbon intensity mobility to the legacy fleet and will become more important in shipping and aviation in the future. Total GHG emissions— from biomass feedstock production, through feedstock conversion to biofuel, and to the latter’s use in internal combustion engines (ICE)—are typically between 32% and 98% lower than those resulting from the use of fossil fuels such as gasoline, diesel, and natural gas. Biodiesel, bioethanol, and hydrotreated vegetable oils (HVO) are already widely used and provided some 3% of transport energy globally in 2017 (Renewables 2020 Global Status Report). In comparison, renewable electricity provided only 0.3% of transport energy in 2017.

Transport biofuels can significantly reduce GHG emissions of the current fleet (Photo credit:Pexels/ Roman Odintsov)

There are already technologies for producing biofuels based on forestry and agricultural residues and waste materials, and these continue to be improved through research and development. The production costs of transport biofuels are usually higher than those of fossil fuels. Their market introduction and use typically depend on dedicated supportive policy measures. While battery electric vehicles are expected to gradually replace light-duty vehicles powered by an internal combustion engine (ICE), long-distance and heavy-duty transport are harder to electrify. That is why after 2030 biofuels are expected to be primarily used in aviation, shipping, and heavy-duty road transport (trucks) rather than in light-duty vehicles.

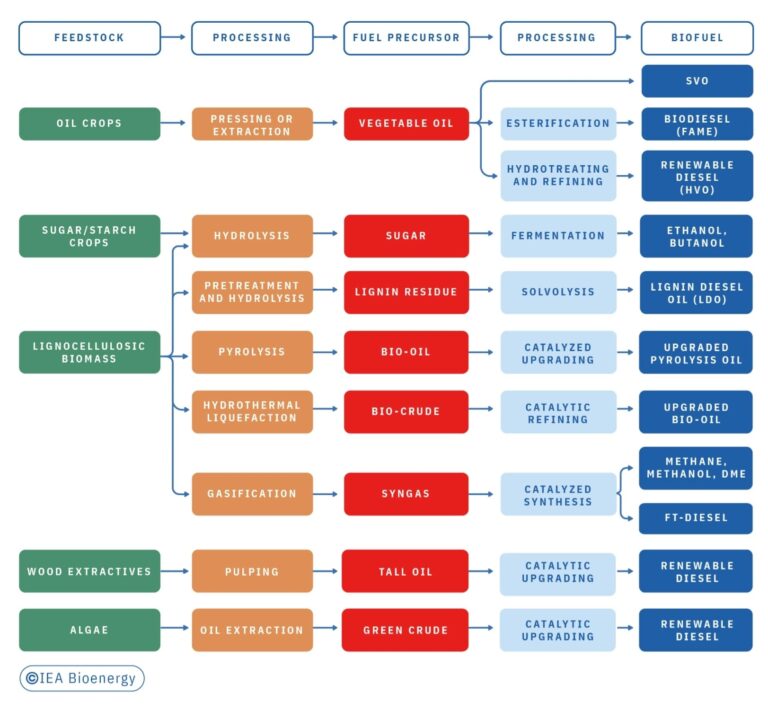

Feedstocks for the production of transport biofuels include oil-seed crops, sugar and starch crops, lignocellulosic agricultural and forestry residues, and wastes such as straw, corn cobs, wood chips, wood extractives from pulping processes, and even water-based plants such as micro- and macroalgae. A wide range of mechanical, chemical, thermochemical, and biochemical processing steps are applied to convert these feedstocks into transport biofuels (The Role of Renewable Transport Fuels in Decarbonizing Road Transport – Production Technologies and Costs).

Several synthesis technologies used for the production of transport biofuels can also be applied using renewable, low carbon intensity hydrogen produced through electrolysis and recovered or captured CO2 as feedstock; such fuels are called e-fuels (electrofuels) or power-to-x fuels. Examples of potential e-fuels include methane, methanol, and upgraded Fischer-Tropsch liquids.

Technology readiness level and status of implementation

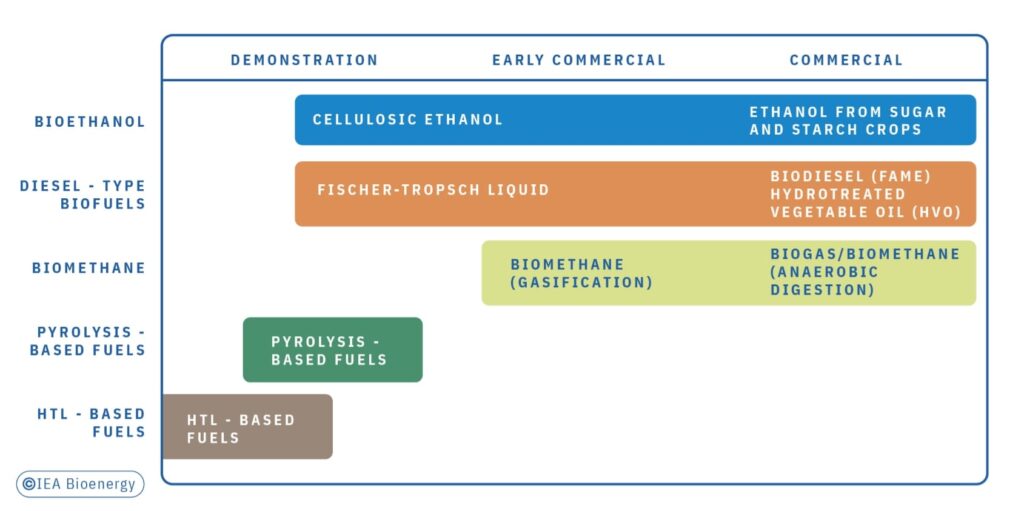

In the case of transport biofuels, a number of production technologies have reached maturity, are already at TRL 9, and are widely deployed. These so-called established biofuels include ethanol from sugar and starch crops, biodiesel from triglycerides and lipids (FAME), hydrogenated triglycerides and lipids (HVO), and biomethane from upgrading of anaerobic digestion biogas.

Energy demand in the transport sector is unevenly split across transport modes. In 2019, global road transport used the major share (42% in trucks and 35% in cars), while maritime transport used 13%, aviation 7%, and other transport, including rail, only 3%.

Currently, transport biofuels are mostly consumed in light duty road transport, supporting the decarbonisation of the sector. In future decades, when electrification is expected to power significant shares of light duty road transport, biofuel use will remain important but is likely to refocus on powering sectors that are harder to electrify. Research has thus started to address the issue of providing biofuels to maritime transport and aviation.

Road transport

Ethanol, biodiesel (FAME), and HVOs are the most common biofuels used in the road transport sector. While, initially, several automakers allowed the use of neat biodiesel (FAME) in their vehicles, they no longer do so due to its poor cold flow properties and problems in modern exhaust gas after-treatment systems. Instead, biodiesel (FAME) is blended with diesel fuel at levels of, for example, 5%, 7%, 10%, 20%, and 30%.

Ethanol is most commonly used as a low-level blending component with gasoline at levels of, for example, 5%, 10%, 15% , and 27%. Ethanol can also be used in adapted drive trains in so- called flex-fuel vehicles at a level of 85%. In Brazil, thanks to favourable climatic conditions and specially developed vehicles, ethanol is also being used in hydrous form (~95% ethanol, ~5% water).

HVO, as well as upgraded paraffinic fuel produced through Fischer-Tropsch synthesis, is a so- called drop-in fuel that can be fully substituted for fossil diesel. To date, due to restrictions in the diesel standard, the most common use of HVO is as a 30% blend with fossil diesel. The use of pure HVO, for example by freight companies wishing to decarbonise is, however, becoming more common.

Biomethane is another example of a drop-in fuel that can be used directly in natural gas vehicles as a substitute for (fossil) natural gas. A range of other biofuels is under investigation, including methanol, butanol, dimethyl ether (DME), and other ethers. These fuels are likely to require fuel-related adaptions to the drive train, lubricants, and exhaust after-treatment systems.

It should be noted that although low-level blending of biofuels is efficient for quickly reducing GHG emissions and building a market for biofuels, high decarbonisation targets can be achieved only with high-level blends or neat biofuel applications.

Shipping

International merchant shipping is responsible for transporting more than 80% of goods worldwide. Shipping is the least carbon intensive mode of transport (expressed as per tonne- km) and produces only 2–3% of global GHG emissions. International shipping vessels are, however, traditionally fuelled with heavy fuel oil (350 million tonnes per year). This high energy density but very low-quality fuel has a high sulphur content, making shipping the largest source of anthropogenic sulphur emissions and a significant emitter of nitrogen oxides and airborne particle emissions.

The International Maritime Organization (IMO) has the target of decreasing the carbon intensity of the shipping sector by 50% by 2050 and mandating new ships to increase energy efficiency. The maximum allowed sulphur content of marine fuels was reduced from 3.5 wt.% to 0.5 wt.% in 2020. This significant drop in sulphur content does not, however, allow the continued use of high-sulphur heavy fuel oil unless scrubbers are used to clean the exhaust gas. International shipping companies are thus looking into alternative solutions.

Sustainable biofuels are among the most promising short- to medium-term solutions for reducing both GHG and sulphur emissions from shipping transportation. A range of feedstocks and biofuel production technologies could be used to produce marine biofuels, and the best solution for each case depends on local parameters such as distance to major fuel hubs, carbon pricing and other supportive policy measures, and availability of biomass.

The main barriers to the implementation of marine biofuels are the lack of economic incentives and the high level of uncertainty related to price development of biofuel feedstocks, sustainability criteria, and regulatory policies. This underlines the importance of supportive and stable long- term policies for triggering investments in alternative marine fuel development and deployment. Establishing supply chains or adapting engine and fuels systems to biofuels seem to be of relatively little concern, according to interviews with key shipping sector stakeholders.

However, the current marine fuel standard or specification includes parameters that cannot be met by many prospective marine biofuels, thus obstructing their use, trade, and production. To accelerate the adoption of sustainable biofuels for marine applications, we would need to revise marine fuel standards, but that will require time and successful demonstrations using large volumes of marine biofuels; this would impose high costs on marine biofuel development and deployment. In the interim, technical reports such as the IMO interim guidelines on using ethanol and methanol as marine fuels, approved in November 2020, can help support this transition.

Aviation

While the aviation sector currently accounts for only 2% of global CO2 emissions, it is predicted to expand further; stakeholders have committed to carbon neutral growth after 2019 and to achieve carbon neutrality by 2050. Measures to achieve future reductions in GHG emissions include more efficient aircraft, improved air traffic management, offsetting of GHG emissions, and the use of low carbon intensity fuels.

Although biojet fuels produced by a variety of production pathways have been approved for use in aviation, hydrotreated esters and fatty acids (HEFA)–Synthetic Paraffinic Kerosene (SPK) fuels provided the vast majority of biojet fuel used in 2021. HEFA-SPK biojet fuel is anticipated to dominate the aviation biofuels market for at least the next 10–15 years. Approximately 150 million litres of biojet fuels were produced globally in 2021, which represents less than 0.5% of total jet fuel demand. As the volume of suitable feedstock (oils and fats) for the HEFA process is limited, it is important to develop further production pathways that can make use of more abundant renewable feedstocks.

The certification process for new biojet fuel production pathways is lengthy and requires relatively high volumes of fuels for testing. This imposes high costs on biojet fuel development and deployment. These costs, along with a range of technological challenges, constitute a significant barrier to the commercialisation of new production pathways.

Current biojet fuels cost several times more than their fossil counterparts, making their use economically unattractive. Costs may decrease, for example, through improvements to the biojet fuel production process, yet supportive policies will be essential to both create market demand and to further catalyse biojet fuel development.

Environmental effects

Major drivers for introducing transport biofuels around the globe include their use as a substitute for fossil fuels, improved energy security, reduced GHG emissions, and increased rural incomes. When the environmental effects of biofuels are analysed, the focus is typically on the impacts of GHG emissions and fossil energy use. There are, however, other important negative environmental and health effects to take into account, such as acidification, eutrophication, human toxicity, ecological toxicity, biodiversity, and water and land footprints, which are less well studied and deserve attention.

Life-cycle assessments (LCA) range from the cultivation or collection of biomass feedstock, to harvest, storage, and transportation, then conversion to biofuel and distribution to the end consumer, to the final use of the biofuel in the engine. All resources used and energy inputs required along the value chain are considered, and all resulting GHG emissions counted. CO2 released from the final fuel combustion process is credited as biogenic CO2 rather than fossil- derived CO2; these biogenic CO2 emissions are equivalent to the amount of atmospheric CO2 taken up by the plant biomass during growth. Resulting GHG emissions are allocated to the final product and by-products, with different default allocation methods being used by different LCA tools and studies.

Important GHG emission calculation tools for transport biofuels include GREET (USA); GHGenius (Canada); the methodology prescribed in the EU Renewable Energy Directive; Virtual Sugarcane Biorefinery (VSB, Brazil); and Open LCA. Due to variations in the underlying datasets for feedstock cultivation and processing, regional variations—in, for example, fertiliser type, application amount and timing, and the choice of allocation method—different biofuel LCAs sometimes can, and do, produce different and even widely conflicting results. A number of reports have been produced to explain the variations in results for different biofuel LCA studies and to help policymakers understand the sensitivities and findings of transport biofuel LCAs. It is important to understand that LCAs do not deliver point values but value ranges, and that they should serve to identify levers for improvements along the processing chains.

In the USA and the EU, renewable fuels have to reduce GHG emissions by at least 20% and 65%, respectively, if produced in new installations; in both regions, therefore, biofuels over their life- cycle have to produce fewer GHG emissions than fossil fuels typically do. Biofuels that are based on wastes or residues typically achieve high GHG emission reductions (80% or higher). Some production pathways even offer the potential to achieve negative emissions, for example, when emissions resulting from the decomposition of untreated wastes are avoided through conversion of the wastes into biofuel or when CO2 emissions from the production process are captured and stored (CCS). Typical values for GHG emissions of various pathways can be found, for instance, in Annex V of the EU Renewable Energy Directive recast.

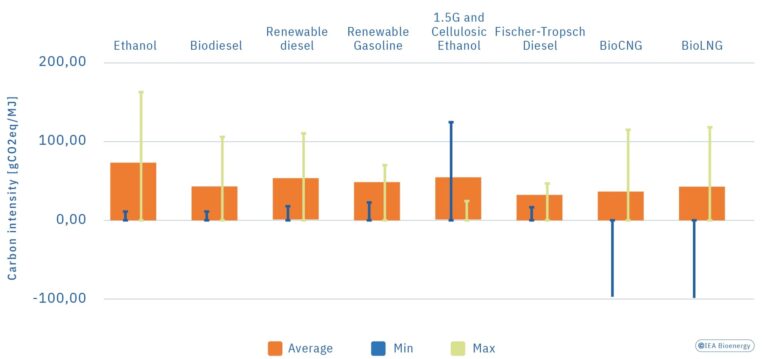

Another way of measuring is to calculate the carbon intensity (CI) of fuels, as this represents the net GHG emissions emitted across the full life cycle of the fuel. For comparison, the carbon intensities of producing and using fossil gasoline or diesel are about 95 gCO2eq/MJ. Real-life values for the carbon intensity of biofuels provided for California in 2019 are well below the carbon intensity of fossil fuels.

As policies based on actual GHG emission reductions of biofuels (like Low Carbon Fuel Standard (LCFS) policies) become more common across the world, the CI of current and emerging biofuels is expected to decrease, for example, through the increased use of wastes and biomass residues as raw materials. This will reduce or avoid the use of fossil fuels to supply energy for production plants and the ongoing technological learning will result in the realisation of larger-scale processing facilities that achieve greater economies of scale. There is also a strong potential in many locations to improve plant efficiencies and reduce costs through more widespread implementation of industrial symbiosis in biofuel production plant design.

Costs

The costs of producing transport biofuels are usually higher than the price of the fossil fuels for which they are being substituted, making their production uneconomic in the absence of policy measures to support production. There is potential to reduce these costs by using lower- cost feedstocks and other input materials such as enzymes, thereby enhancing the conversion efficiency or improving the monetisation of co-products. Technology developers and biofuel producers across the globe are exploring these avenues. For example, the recent capacity increase for the production of hydrotreated vegetable oil- (HVO)-type fuels is being driven by several regions such as Sweden and California which are economising on production costs through a combination of using low-cost feedstocks and production incentives, and also through carbon credits markets created by LCFS policies.

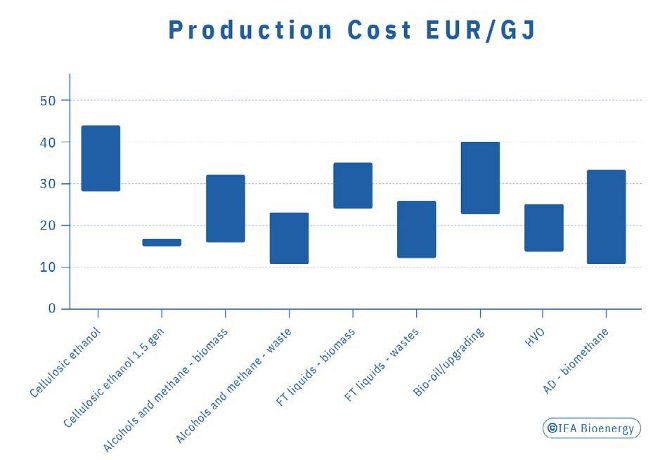

Other production routes, especially those using lignocellulosic materials such as wood or straw as raw material, that require collection and transport, are still uneconomical. To better understand and communicate the scope to reduce the production costs of such biofuels, IEA Bioenergy published a study entitled “Advanced Biofuels – Potential for Cost Reduction”. The study illustrates that it is difficult to develop and demonstrate these technology pathways, as the investment required is about 5–10 times higher than for established biofuels like HVO or conventional ethanol, depending on the conversion pathway.

The IEA study also demonstrates that feedstock costs and capital costs are the major contributors to overall biofuel production costs. It finds that production costs using biomass feedstocks that must be collected and delivered lie in the range of 17–44 EUR/GJ and are reduced to 13–29 EUR/ GJ if wastes are used as feedstocks. This compares with a range of fossil fuel prices of 8–14 EUR/GJ in 2019, when the assessment was carried out. There are early market opportunities for producing lower-cost advanced biofuels from wastes and through integration of advanced biofuel production with existing biofuel processing plants. As a side note, fossil fuel prices have increased significantly since the above assessment was carried out, from around 60 USD/barrel in 2019, through a low in early 2020 at <20 USD/barrel, up to a spike of >120 USD/barrel in early 2022.

Further cost reductions can be achieved through technology learning from demonstrations that reduce investment costs, and also through cheaper access to capital as the perceived investment risk decreases. In addition, carbon pricing can help to bridge the gap between biofuel production costs and the price of fossil fuels.

Current research gaps and opportunities

Biofuel production pathways are at different technology readiness levels, and R&D needs vary according to feedstock, conversion technology, and technological maturity. Many publications provide insights and guidance on where to focus research and development efforts to make further advances in biofuels. Examples of such publications include the following:

- IEA Biofuels Technology Roadmap (2011)

- IRENA Advanced Liquid Biofuels (2016)

- IEA Bioenergy Technology Roadmap (2017)

- ETIP Bioenergy Strategic Research and Innovation Agenda (2018)

- IRENA Advanced Biofuels – What holds them back (2019)

Although these publications were written several years ago, the majority of technology-specific challenges they describe remain valid. A selection of R&D needs for important transport biofuel pathways is presented below.

Biogas

(see also chapter 10 Biogas production for heat, electricity, renewable gas, and transport)

Specific R&D needs include the development and demonstration of feedstock pre-treatment to enhance gas yield and allow processing of recalcitrant materials and the development and demonstration of improved technologies for biogas production and upgrading to biomethane. The use and valorisation of digestate needs to be improved, and conventional biogas facilities should be upgraded to integrated biogas-based biorefineries that efficiently co-produce biofuel

precursors (fatty acids, biogas) and bio-based products.

Lignocellulosic ethanol, higher alcohols, hydrocarbons

Specific R&D needs include:

- the development of improved feedstock pre-treatment and conversion processes (less intense use of water, energy, chemicals, and enzymes) to improve process efficiency and product titre;

- the development of novel strains to produce hydrocarbons or long-chain fatty alcohols from sugars;

- the development and demonstration of improved separation technologies (e.g., ethanol recovery from fermentation broth or avoidance of product inhibition through continuous removal of products);

- the development of lignin valorisation towards energy/fuels and bio-based products.

Gasification

(see also chapter 8 Gasification for multiple purposes)

Specific R&D needs include: i) feedstock pre-treatment for, and feedstock flexibility in, primary conversion; ii) the development and demonstration of improved gas cleaning (e.g., hot gas cleaning) and upgrading; iii) the demonstration of hybrid renewable energy power processes; iv) the improvement of catalyst longevity and robustness; and v) the efficient use of low- emperature heat.

Direct thermochemical liquefaction (pyrolysis and HTL

(see also chapter 9 Direct thermochemical liquefaction)

Specific R&D needs include:

- the development of systems with improved intermediate quality (e.g., reduced oxygen content);

- the demonstration of upgrading of intermediate products (including co-processing);

- the improvement of catalysts for all conversion steps.

Opportunities with respect to biofuels include:

- increasing the feedstock flexibility of technologies;

- adapting marine standards to enable wider use of biogenic fuels;

- developing supply chains for providing and bunkering biofuels for ships and planes;

- enabling the co-processing of bio-oils and bio-crudes in petroleum refineries;

- developing carbon capture technologies compatible with the size of typical biofuel production

facilities.

Earlier hopes that large quantities of biofuels could be produced based on aquaculture of algae, thus not requiring fertile land for cultivation of the raw material, have not materialised; the higher costs of cultivating and harvesting algae compared to other biomass feedstocks require higher- value (i.e., non-fuel or energy) products to be economically viable. Research is still ongoing, focusing on biorefinery approaches with higher value algal biomass-based products providing the critically needed revenue to reduce the net cost of producing algal-based biofuels.

Powerful policy instruments

Supportive policies have been, and will continue to be, essential to foster the growth of the advanced biofuels used to decarbonise transport. To date, most policies have focused on road transport. Other transport sectors, such as rail, aviation, and shipping, have, until recently, received comparably less attention, despite being large energy consumers and GHG emitters. Transport policies and industry efforts are, however, being increasingly extended to focus on decarbonising long-haul transport sectors (i.e., road, rail, aviation, and shipping), where electrification is much more challenging.

The market introduction of biofuels and the development of even more efficient biofuel production technologies should be supported by a well-balanced basket of policy measures and long-term, stable policy commitment. Policy tools that have been successful include blending mandates, excise tax reductions or exemptions, renewable or low carbon fuel standards, and a variety of fiscal incentives and public financing mechanisms. There are two main policy types: technology- push policies, that aim to drive early-stage technology development through RD&D support, and market-pull policies, that help create demand for established or technically more mature transport biofuels.

Within the basket of successful policy tools, biofuel blending mandates are the most widely adopted (e.g., in Brazil, Canada, Japan, South Korea, United States, and the EU. In most cases these blending mandates are based on the volume or energy content requirements, and thus effectively support the use of biofuels that can be produced at the lower end of the production cost range: they are, however, less effective in terms of stimulating the development and deployment of higher production cost biofuels that achieve even lower carbon intensities.

The first policy to introduce carbon intensity (CI) as a measure for incentivising biofuels was the 2007 Low Carbon Fuel Standard (LCFS) of the state of California (USA). LCFS-type policies encourage the more efficient production of established biofuels and also stimulate the development and deployment of biofuels that offer higher GHG emission reductions by increasing their market value. These types of carbon intensity–based policies are becoming more common. As of late 2021, the states of California, Oregon, and Washington in the United States, the province of British Columbia in Canada, Brazil, Germany, and Sweden have all implemented such LCFS-type policies, and many other regions (e.g. Canada with its upcoming Clean Fuel Standard) are also considering doing so.

Pan-national regulations are important in terms of driving the introduction of alternative fuels in sectors like aviation and shipping. For the aviation sector, the International Civil Aviation Organisation’s Carbon Offsetting and Reduction Scheme for International Aviation (ICAO CORSIA) sets the global aspirational goal of keeping the global net carbon emissions from international aviation at the same level from 2020 onwards. To achieve this goal, an important element is the use of sustainable aviation fuels. In November 2021, ICAO published its Sustainability Criteria for CORSIA Eligible Fuels and Default Life Cycle Emissions Values for CORSIA Eligible Fuels. While ICAO has no right to make regulations, it convenes its 193 members and supports them in setting up regulations to reach this aspirational goal. The proposed ReFuelEU Aviation Directive is an example of a (regional) regulation of this kind.

For the shipping sector, the International Maritime Organization (IMO), which is responsible for measures to prevent pollution from ships, has adopted two distinct regulations that make biofuels advantageous for the shipping sector. The first is the so-called IMO 2020 that sets a new limit on the sulphur content of the fuel oil used on board ships. The second is the Initial IMO. Strategy on reduction of GHG emissions from ships. The strategy sets a framework for national and regional regulations, such as the proposed FuelEU Maritime Directive.

Biofuel-specific R&D funding programs and investment support for demonstration facilities are an important element in stimulating the research, development, and demonstration of emerging biofuel technologies.

Countries that use a mixture of market-pull and technology-push policy instruments have been the most successful in terms of increasing biofuel production and use and also at developing and deploying fewer mature emerging biofuel production technologies. To further expand the production and use of transport biofuels, it will be important to establish long-term policy support comprising a well-balanced and adaptable basket of policy measures, including safeguards for sustainable production and consistent regulation in the global trade of biofuels.

An overview of biofuel policy tools applied in 15 countries and the European Union is provided in “Implementation Agendas: 2020-2021 Update – Compare and Contrast Transport Biofuels Policies”.

- Horizon 2020 Work Programme 2014- 2015 – General Annexes -Annex G Technology readiness levels (TRL) LINK accessed 18/02/2022

- IEA Bioenergy Task 39 Database on facilities for the production of advanced liquid and gaseous biofuels for transport LINK accessed 18/02/2022

- IEA Bioenergy Task 37 (2021) Perspectives on biomethane as transport fuel within a circular economy, energy, and environmental system LINK accessed 23/06/2022

- IRENA (2021) Innovation Outlook: Renewable Methanol LINK accessed 23/06/2022

- IEA Bioenergy Task 39 (2021) Progress towards biofuels for marine Shipping Status and identification of barriers for utilization of advanced biofuels in the marine sector LINK accessed 18/02/2022

- IMO International Maritime Organization (2020) Interim guidelines for the safety of ships using methyl/ethyl alcohol as fuel LINK accessed 18/02/2022

- ATAG Air Transport Action Group LINK accessed 18/02/2022 IEA Bioenergy (2020) The Role of Renewable Transport Fuels in Decarbonizing Road Transport LINK accessed 18/02/2022

- REN 21 Renewables Now (2020) Renewables 2020 global status report LINK accessed 18/02/2022

- IEA Bioenergy Task 39, LINK accessed 23/06/2022

- Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the promotion of the use of energy from renewable sources LINK accessed 18/02/2022

- IEA Bioenergy (2020) The Role of Renewable Transport Fuels in Decarbonizing Road Transport LINK accessed 18/02/2022

- IEA Bioenergy Task 39 (2022) Implementation Agendas: Compare-and-Contrast Transport Biofuels Policies (2019-2021 Update) LINK accessed 22/06/2022

- IEA Bioenergy (2020) Advanced Biofuels – Potential for Cost Reduction LINK accessed 18/02/2022

- IEA Technology Roadmap Biofuels for Transport (2011) LINK accessed 18/02/2022

- IRENA International Renewable Energy Agency (2016) Outlook advanced liquid biofuels LINK accessed 18/02/2022

- IEA (2017) Technology Roadmap Delivering Sustainable Bioenergy LINK accessed 18/02/2022

- ETIP Bioenergy (2018) Strategic research and innovation agenda LINK accessed 18/02/2022

- IRENA International Renewable Energy Agency (2019) ADVANCED BIOFUELS What holds them back?LINK accessed 23/06/2022

- IEA Bioenergy (2017) State of Technology Review – Algae Bioenergy LINK accessed 23/06/2022

- Government of Canada, What is the clean fuel standard? LINK accessed 23/06/2022

- ICAO (2019) Resolution A40-19: Consolidated statement of continuing ICAO policies and practices related to environmental protection – Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) LINK accessed 23/06/2022

- ICAO, Sustainable Aviation Fuels (SAF) LINK accessed 23/06/2022

- ICAO (2021) CORSIA Sustainability Criteria for CORSIA Eligible Fuels LINK accessed 23/06/2022

- ICAO (2021) CORSIA Default Life Cycle Emissions Values for CORSIA Eligible Fuels LINK accessed 23/06/2022

- European Parliament (2022) ReFuel EU Aviation initiative Sustainable aviation fuels and the fit for 55 package LINK accessed 23/06/2022

- IMO (2020) Cutting sulphur oxide emissions, LINK accessed 23/06/2022

- IMO (2020) Greenhouse Gas Emissions LINK accessed 23/06/2022

- Eurepean Parliament (2022) Sustainable maritime fuels ‘Fit for 55’ package: The Fuel EU Maritime proposal LINK accessed 23/06/2022

- IEA Bioenergy Task 39 (2022) Implementation Agendas: Compare- and-Contrast Transport Biofuels Policies (2019-2021 Update) LINK accessed 22/06/2022

FURTHER READING

- IEA Bioenergy Task 39 (2011) Biodiesel GHG emissions, past, present, and future LINK accessed 18/02/2022

- IEA Bioenergy Task 39 (2013) Advanced Biofuels – GHG Emissions and Energy Balances LINK accessed 18/02/2022

- IEA Bioenergy Task 39 (2012) Life Cycle Analysis of transportation fuel pathways LINK accessed 18/02/2022

- IEA Bioenergy Task 39 (2017) Comparison of Biofuel Life Cycle Assessment Tools LINK accessed 18/02/2022

- Pereira LG, Cavalett O et al. (2019) Comparison of biofuel life-cycle GHG emissions assessment tools: The case studies of ethanol produced from sugarcane, corn, and wheat” Renewable and Sustainable Energy Reviews 110,1- 12 LINK

- IEA Bioenergy Task 39 (2018) Comparison of Biofuel Life Cycle Analysis Tools Phase 2, Part 1: FAME and HVO/ HEFALINK LINK accessed 18/02/2022

- IEA Bioenergy Task 39 (2019) Summary Series, Comparison of international Life Cycle Assessment (LCA) biofuels models LINK accessed 18/02/2022

- IEA Bioenergy Task 39 (2019) Comparison of Biofuel Life Cycle AnalysisTools Phase 2, Part 2: biochemical 2G ethanol production and distribution LINK accessed 18/02/2022